Summary

The Most Important Thing is a collection of essays and reflections about investing and markets through Marks’ career as a value investor. Marks is a strong believer in the reality that markets can be inefficient, that contrarian thinking is the only way to beat the market, and that understanding where we are in the credit cycle is imperative for long-term survival. Beating the market over the long term is not easy, but by staying unemotional, thinking one step ahead and being patient, it is possible. The book shares lessons and frameworks for how to do just that.

Takeaways

I studied economics in university, which means I learned the empirically tested idea that you cannot beat the market. The efficient market hypothesis says prices reflect all available information, meaning that over time, no investor can hold an edge long enough to consistently outperform. In classrooms this is a law, not a debate. Yet in reality, Warren Buffett happened, Howard Marks happened. There are decades of documented outperformance by a select few.

If the theory is right, the evidence shouldn’t exist. If the evidence is real, the theory is incomplete. So which is it? And what does that gap mean for how you should actually invest if beating the market is on your to-do list?

Why The Market Is Wrong

Between January 2000 and September 2001, Yahoo traded on the NASDAQ at an all time high of $118 and an all time low of $8. So while the business remained largely the same over that period, in hindsight we can clearly see that neither price was justified. The market was therefore wrong, at least once. Not in a theoretical sense. Wrong on the price tag itself.

The dot-com bubble is one of the clearest examples of why markets make mistakes: narrative. Humans are story creatures. We try to explain our past and our futures with meaningful arcs of facts and speculation so that the infinite chaos of the universe makes sense. And the market, being a collective of humans, prices stories more than it prices businesses. When everyone believes the same story, the price reflects that belief rather than the underlying value. And since narratives are most compelling at their peak, when you’ve just seen prices rise beyond what anyone expected, they are also most persuasive at the worst moment. This is how people lose money. But on the flip side, the most undervalued assets tend to look their worst at bottom, when their ugly narratives look most perverse.

This creates a third problem; one that I’ve found fascinating since I read about it in Thinking In Bets several years ago: You cannot learn from results. Just as a successful outcome doesn’t necessarily mean you made a wise decision, a stock that went up after you bought it does not mean the purchase was wise. While economics textbooks define risk as volatility, Marks describes it in a more useful and intuitive way: the probability of loss at the moment of decision. Lucky outcomes do not retroactively reduce that probability and unlucky outcomes don’t retroactively increase it. Risk is tough to gauge in the moment, but what we do know is that even the most data-backed financial models impose assumptions about the future that are fundamentally also just a story.

What Risk Actually Is

Once you accept that risk is just the probability of loss, and that prices and real value can diverge for extended periods of time, the nature of risk becomes a lot clearer. Risk is not a property of an asset. Apple as a business has no risk. Risk is a property of the price you pay relative to the value you receive. When the market is bullish, prices are pushed up above value, and the gap between price and value is where the risk lives. According to Marks, the simplest form of risk management then is not a diversification strategy, or a stop-loss rule. It is just the discipline to avoid overpaying.

That sounds a lot easier than it is in reality. Like most investing concepts, there is a humbling caveat attached. Identifying an overpriced market or asset does not mean you have identified a correction. In other words, over priced does not mean going down tomorrow. Markets can stay wrong for much longer than any rational model would suggest. An overpriced market can continue to rise for years. That is why standard advice is to just buy the index. Timing the market is too hard; you have to be right twice, once on direction and once on timing. Even if you’re right on the first, you’re likely to miss badly on the second.

How To Win: Second Level Thinking

If prices are driven by consensus, then earning returns above the market requires disagreeing with consensus in ways that turn out to be right. This is what Marks calls second-level thinking. The first level investor asks whether the company is good or bad. The second-level investor asks what the consensus already expects, how the current price reflects that, and what happens to the price if the consensus is wrong.

I’m going to walk through an example here, but I want to make clear beforehand that this is not investment advice and I do not own shares in the company below at the time of writing.

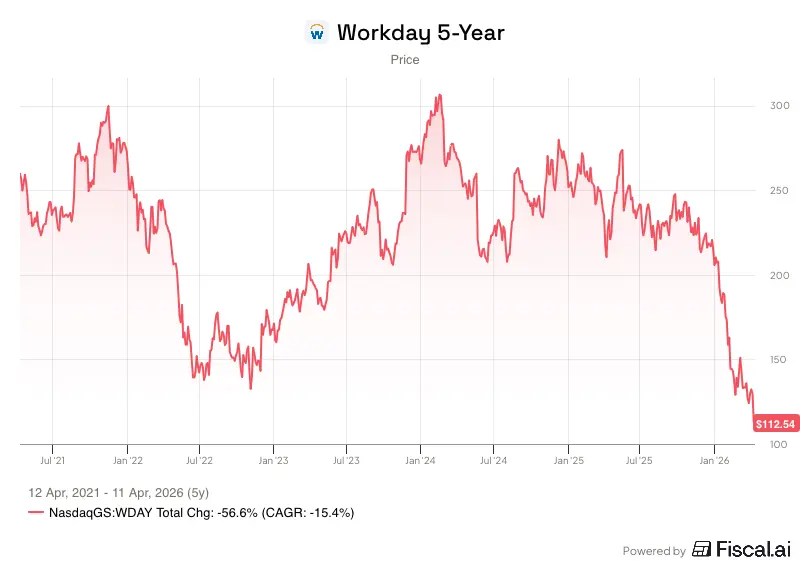

Take a look at the Workday stock below.

Like many SAAS businesses, it’s down over 50% from its highs. As Anthropic, OpenAI and Google release increasingly powerful AI models, the narrative that agentic AI will render enterprise software obsolete is hammering the industry stock prices.

First-level thinking takes the fear at face value. Second-level thinking asks whether Proctor & Gamble, KPMG, and Walmart actually want to build and maintain custom HR software in-house. Does the economic logic of outsourcing IT infrastructure disappear just because the underlying code is generated differently? If it does not, the narrative fear might be overstated in the price.

The other thing second level thinking implies is that the market temperature should be considered as well before acting. Marks provides a framework. Ask whether the economy is vibrant or sluggish. Whether lenders are eager or hesitant. Whether other investors are optimistic or distressed. Whether asset prices are high or low. Whether capital markets are loose or tight. In the words of Marks, if most of your answers cluster in the left column, hold onto your wallets.

I built a skill for Claude to do exactly this and here is the output:

Howard Marks Market Temperature — April 2026: 13 Left, 5 Split, 4 Right

| Pair | Reading | Evidence |

|---|---|---|

1. Economy Vibrant ↔ Sluggish | Split | US GDP tracking ~2% growth; recession probability ~30–40% and rising. Growth increasingly concentrated in AI-capex, other parts of the economy strained. |

2. Outlook Positive ↔ Negative | Left → shifting | McKinsey survey: for the first time since late 2022, more respondents expect global conditions to worsen than improve. 70% of executives rank a recession scenario as most likely. |

3. Lenders Eager ↔ Reticent | Split | Bank lending conditions technically solid per the St. Louis Fed. But HY spreads showing early signs of widening and leveraged buyout debt capacity contracting from 6x toward 4.5x. |

4. Capital markets Loose ↔ Tight | Left | Financial conditions "broadly accommodative" despite geopolitical stress. Investment-grade deals being oversubscribed 5x. IG spreads hit multi-decade tights near 71 bps at January peak. |

5. Capital Plentiful ↔ Scarce | Left | Q1 2026 was the biggest VC/PE fundraising quarter since 2021 — $80B+ in a single quarter. PE dry powder at ~$1.1 trillion. AI funds commanding record commitments. |

6. Terms Easy ↔ Restrictive | Split | Investment-grade terms remain easy; leveraged and lower-quality transactions face tighter structures and reduced multiples. Credit markets shifting "from abundance to selectivity." |

7. Interest rates Low ↔ High | Right | Fed funds at 3.5–3.75%, held steady for 2 consecutive meetings. A senior Fed official signaled rates could rise again if oil-driven inflation persists. Only one cut expected in all of 2026. |

8. Spreads Narrow ↔ Wide | Left | IG spreads near multi-decade tights (below 83 bps at points, last seen in 1998). HY at ~3%, below their 20-year average of 4.9% — near 2007 levels. Widening is the more likely next move. |

9. Investors: mood Optimistic ↔ Pessimistic | Split | Institutional investors gradually withdrawing from US equities even as retail pours in. AI cycle confidence coexisting with recession fears. PwC describes markets as "stubbornly complacent" about policy risks. |

10. Investors: composure Sanguine ↔ Distressed | Left | Despite the April 2025 tariff shock, markets proved resilient — 2025 delivered strong public market returns. Risk assets remain elevated. Volatility present but not crisis-level. |

11. Investors: intent Eager to buy ↔ Uninterested | Left | $80B+ Q1 fundraise; retail pouring into US equity ETFs; IPO pipeline actively building. M&A surged 40% YoY in 3Q25. Record inflows into IG bond ETFs. |

12. Asset owners Happy to hold ↔ Rushing for exits | Left | PE holding periods extended (median 6.1 years) but not crisis-driven — sponsors choosing to hold pending favorable exit conditions, not forced sellers. 2025 exit rebound was orderly. |

13. Sellers Few ↔ Many | Left | IPO market reopening selectively; no widespread forced selling. Institutional sellers in equities are gradual, not urgent. Secondaries market growing as active portfolio management, not distress. |

14. Markets Crowded ↔ Starved for attention | Left | US equities and AI infrastructure intensely crowded. M7 valuations near top 10% of historical distribution. Non-AI sectors struggling to attract funding. |

15. Funds: access Hard to enter ↔ Open to anyone | Left | Top-tier VC/PE funds oversubscribed; several raised at or above hard caps with one-and-done closes. The top 5 VC funds alone took $35B+ in Q1 2026. Access to marquee managers as restricted as any point since 2021. |

16. New funds Daily launches ↔ Only best can raise | Split | Marquee and AI-focused managers raising record amounts; institutional fundraising drought otherwise continued through 2025 (weakest year since 2017). Emerging managers fighting for what's left. |

17. GP/LP power GPs hold cards ↔ LPs have power | Left | Top GPs dictating terms on oversubscribed raises. Massive AI-focused funds setting their own timelines. LPs have some leverage in secondaries but overall power sits firmly with top GPs. |

18. Recent performance Strong ↔ Weak | Left | 2025 delivered strong public market returns despite the April tariff shock. US equities hit new all-time highs. Strong earnings from tech/AI anchored the rally. PE exits rebounded strongly in 2024–25. |

19. Asset prices High ↔ Low | Left | M7 P/E multiples near top 10% of historical distribution. IG credit spreads below 1998 levels. HY spreads at a 2007 analog. Equities offer little margin of safety at current multiples. |

20. Prospective returns Low ↔ High | Left | Fixed income offers 6%+ yield but credit upside is spread-compression-limited. Equity upside constrained by historically high starting multiples. BlackRock: "investors should respect the potential for gravity to assert itself." |

21. Risk level High ↔ Low | Right ↗ | Energy shock from the US-Iran conflict introducing stagflationary risk. Fed policy trap: fighting oil-driven inflation while growth slows. Fed chair transition adding institutional uncertainty. Tail risks have materially grown. |

22. Popular quality Aggression & reach ↔ Caution & selectivity | Right ↗ | BlackRock, PinesBridge, and Schwab all shifting language toward "selectivity," "up-in-quality," and "caution." Rhetoric moving from 2024's risk-on consensus toward defensive posturing — even if allocations haven't fully followed yet. |

Firmly on the side of risk. Buffett might say “Be greedy when others are fearful, and fearful when others are greedy.” But Marks makes another important point on fear as well. The more subtle and pernicious side of fear does not manifest in panic selling, but rather paralysis. You watch prices fall and tell yourself to wait until things are clearer, until the bottom is in. But things are never clearer at the bottom. The narrative is always worst exactly when the price is most attractive.

The fact is that, as discussed above, even a well-reasoned position can go against you for months or years. An undervalued stock can fall further. The antidote to panic and fear is a rational analysis: not necessarily a quantitative model, but a qualitative thesis, and well-reasoned thesis breakers. That is what gives you the confidence to hold through the discomfort of being early, and separate a signal that you were wrong from emotional noise.

The practical implication of all this is that you don’t need to predict the future. Forward visibility is almost always unclear. All you need to do is read the environment in front of you and let that dictate your posture.

Opportunistic investing is not headline-grabbing, sexy job of hunting for the next big thing. It’s being positioned when a seller is motivated and prices their asset below value. The key is having the patience and emotional stability to let deals come to you rather than manufacturing reasons to act.

The Only Job

There is a concept in tennis called “the pusher”. It’s the word for a certain style of player who likes to sit back, avoid making risky shots, return every ball and simply outlast their opponents mistakes. They are not exciting to watch. But they are effective. The investing equivalent also exists. They read the field in front of them, avoids overpaying, survives the disasters, and deploys capital when prices and value diverge in their favour.

Like opponents in sport, markets can challenge you in gruelling ways that are difficult to prepare for. But they also make mistakes. Those mistakes are not a problem to be solved. It’s the game itself.

Notes

Act On The Present, Not Forecasted Futures

Fear Creates Paralysis, Not Just Selling

High Prices Are The Primary Source Of Risk

Narratives Drive Price, Not Value

Outcomes Don’t Communicate Risk

Overpriced ≠ Going Down Tomorrow